TL;DR

- •Reviewing mortgage statements regularly helps homeowners detect errors, monitor escrow accounts, and understand payment allocations to avoid costly mistakes.

- •Key sections include account details, payment breakdown, loan balance, interest rate, and transaction history, which reveal vital loan information.

Your mortgage statement arrives every month, and if you're like most homeowners, you scan it for the payment amount and move on. That's a costly habit. Understanding mortgage statements in detail means you can catch errors, track your equity, spot escrow problems before they spike your payment, and confirm your lender is applying your money correctly. This guide walks you through every section of a standard statement, explains how your payment is divided, and gives you a practical monthly review process so nothing slips past you.

Model your PITI payment from your statement

Estimate principal, interest, taxes, and insurance to compare against what your servicer reports.

Open Mortgage Payment calculatorKey takeaways

| Point | Details |

|---|---|

| Statements contain six core sections | Federal regulations require account info, payment due, loan balance, interest rate, and payment allocation to appear on every statement. |

| PITI drives your monthly cost | Principal, interest, taxes, and insurance all compose your payment, with early payments weighted heavily toward interest. |

| Escrow shortages are not always tax-related | Under-collections by your lender can trigger escrow shortages and raise your monthly payment unexpectedly. |

| Lender messages deserve attention | Notices buried in the messages section can signal rate adjustments, insurance lapses, or forced-placed coverage. |

| Monthly review prevents costly surprises | Checking each section against your records helps you catch misapplied payments and fee errors before they compound. |

Understanding mortgage statements: key components

A mortgage statement is a monthly document your loan servicer sends to report the current status of your loan. It is not just a bill. Federal regulations require that statements be clear and easy to read, including account number, payment due date, total amount due, current loan balance, interest rate, and a full breakdown of payment allocation. Knowing where to find each item is the first step in reading mortgage statements with confidence.

Here are the core sections you will find on virtually every standard statement:

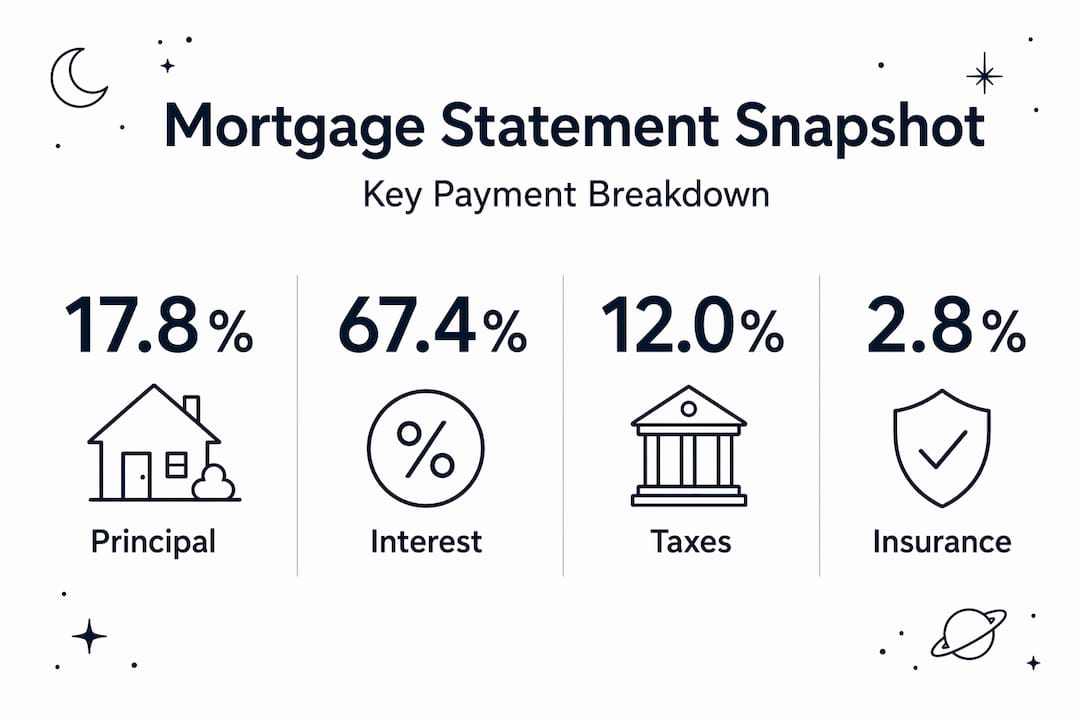

| Payment Component | Amount | Percentage of Payment |

|---|---|---|

| Principal | $320 | 17.8% |

| Interest | $1,100 | 61.1% |

| Escrow (taxes and insurance) | $340 | 18.9% |

| Fees | $40 | 2.2% |

This breakdown is central to the mortgage statement breakdown every homeowner should understand before writing that first check.

- •Account and loan identification. Your name, property address, account number, and loan servicer contact information appear at the top. Confirm these are correct every time. A typo in your account number can cause payment processing issues.

- •Payment due date and total amount due. This line shows exactly what you owe and when. The total may be higher than your base payment if there are past-due amounts or fees rolled in.

- •Outstanding principal balance. This is the remaining loan amount you owe, not counting accrued interest. Watching this number decrease over time confirms your payments are reducing debt as expected.

- •Interest rate. Fixed-rate loans show a single rate that never changes. Adjustable-rate mortgages (ARMs) show the current rate, which may update at each adjustment period.

- •Payment allocation. This line breaks down exactly how your payment is split between principal, interest, escrow, and any applicable fees.

- •Transaction history. A running log of recent payments, dates, and how each was applied. Use this to verify nothing was misapplied.

The following table shows an example of how a $1,800 monthly payment might be allocated on a 30-year fixed mortgage in year three:

How your payment is divided: PITI explained

Monthly mortgage payments consist of four components: Principal, Interest, Taxes, and Insurance. Lenders and financial professionals refer to this combination as PITI. Understanding each part tells you exactly where your money goes and how fast you are building equity.

- •Principal is the portion that directly reduces your loan balance. Every dollar applied to principal builds home equity. In the early years of a 30-year loan, this amount is relatively small.

- •Interest is the cost your lender charges for the loan. Because interest is calculated on the remaining balance, early payments favor interest over principal. As your balance shrinks over time, more of each payment shifts toward principal.

- •Taxes refer to your property taxes, which your servicer collects monthly and holds in an escrow account until the tax bill is due. This prevents a large lump-sum tax payment from catching you off guard.

- •Insurance covers your homeowner's insurance premium and, if applicable, private mortgage insurance (PMI). Like taxes, these funds are held in escrow and paid out when premiums come due.

Equity does not build at a steady pace. In year one of a $300,000, 30-year fixed mortgage at 7%, roughly $20,000 of your payments goes toward interest and only about $4,000 reduces the principal. By year 20, the split flips noticeably. Knowing this helps you decide whether making extra principal payments makes financial sense for your situation. You can model this with a loan payment calculator to see the exact numbers for your loan.

Escrow accounts and annual escrow analysis

The escrow section of your mortgage statement shows three things: the current escrow balance, any disbursements made for taxes or insurance, and a projected surplus or shortage. Most homeowners glance past this section, but it holds some of the most consequential numbers on the page.

Here is how escrow works in sequence:

- Monthly collection. Your servicer collects a portion of your estimated annual taxes and insurance with each payment and deposits it into your escrow account.

- Disbursement. When your property tax bill or insurance premium is due, the servicer pays it directly from the escrow account.

- Annual escrow analysis. Once per year, your servicer reviews the account to confirm collections are keeping pace with actual expenses. If there is a gap, they adjust your monthly escrow amount.

- Surplus or shortage notification. If your account has excess funds, you may receive a refund or credit. If the account is short, your monthly payment increases to cover the difference.

One detail many homeowners miss: escrow shortages can result from previous under-collections by your lender, not just rising property taxes or insurance premiums. If your servicer underestimated your tax bill during the prior analysis, you absorb the difference in the following year's payment adjustment.

Pro Tip: Review the escrow disbursement history on your statement against your actual tax and insurance bills annually. Discrepancies can be disputed. You can also monitor your bills proactively to avoid being blindsided by missed or late escrow disbursements.

How to review your mortgage statement monthly

Reviewing your statement monthly helps you detect errors, payment misapplication, and changes in escrow or fees before they become larger problems. This does not require an accounting background. It requires about ten minutes and a consistent checklist.

Work through these items each month:

- •Verify personal and property information. Confirm your name, address, and account number are correct. Errors here can affect payment posting.

- •Check the payment amount and due date. Compare the total due against last month. Any increase warrants an explanation, usually found in the payment breakdown or lender messages section.

- •Review the payment split. Confirm that principal, interest, and escrow allocations match what you expect based on your loan terms. A drop in principal allocation with no corresponding rate change is a red flag.

- •Monitor the outstanding loan balance. It should decrease with every on-time payment. If it has not moved or has increased, contact your servicer immediately.

- •Scrutinize the transaction history. Verify the exact date your last payment was credited. Regulation X requires servicers to credit payments promptly, and borrowers have the right to file a formal error notice if payments are misapplied or fees are improperly charged.

- •Read the lender messages section. This is where servicers disclose important notices about escrow changes or interest rate adjustments. Ignoring this section can lead to forced-placed insurance or a payment increase you did not see coming.

- •Note any unfamiliar fees. Late fees, returned payment fees, or property inspection fees should be itemized. If you do not recognize a charge, request an itemized fee explanation from your servicer in writing.

If you find something that does not add up, call your servicer with your account number, the statement date, and the specific line item in question. Document the call. If the issue is not resolved, a written error notice triggers a formal investigation under federal servicing rules.

Special considerations: ARMs, modifications, and payoff statements

Most of the time, your statement will look similar month to month. But certain loan types and situations introduce new sections or documents you need to recognize.

- •Adjustable-rate mortgages. ARM statements show your current interest rate, the index it is tied to (such as the Secured Overnight Financing Rate), and the next adjustment date. When a rate change occurs, your statement will reflect the new rate and the revised payment amount. Do not assume your payment stays the same after an adjustment period ends.

- •Loan modifications. If you completed a loan modification, your statement should reflect the new loan terms, including the updated rate, balance, and monthly payment. Verify these match your modification agreement exactly. Discrepancies between the agreement and the statement are something to challenge in writing.

- •Payoff statements. A monthly mortgage statement and a payoff statement are not the same document. A payoff statement shows the exact amount needed to satisfy the loan in full as of a specific date, including accrued daily interest. You must request this separately from your servicer. If you are refinancing or selling your home, request it early since the number changes daily.

My take on what mortgage statements actually tell you

I've spent years looking at financial documents, and mortgage statements are among the most underused pieces of information homeowners have access to. Most people treat them as a reminder to pay. The statement is actually a monthly audit of your loan.

What I've found is that the biggest financial mistakes homeowners make with mortgages are not about rate shopping or down payments. They happen quietly, month after month, when a misapplied payment goes unchallenged or an escrow shortage accumulates unnoticed. By the time someone calls their servicer, they are dealing with months of compounded errors.

The PITI breakdown is where I direct most people first. Once you see how little of your early payments go toward principal, the math behind extra payments becomes undeniable. Even routing an additional $100 per month toward principal in the first five years of a loan has a larger effect on total interest paid than most borrowers realize.

The lender messages section is what most homeowners skip entirely. I've seen cases where forced-placed insurance, which is far more expensive than a standard policy, was added quietly and disclosed only in that section. Reading it takes thirty seconds. Not reading it can cost hundreds.

Your statement is a financial roadmap. Use it like one.

- Michael

Put your mortgage numbers to work with Helpcalculate

Once you understand what your mortgage statement is telling you, the next step is running the numbers yourself.

Helpcalculate offers free financial calculators that pair directly with the concepts in your statement. Use the mortgage payment calculator to estimate your full PITI cost or model a different loan scenario. Want to see how extra payments change your payoff date? The extra payment tool shows exactly how much interest you save by adding even a small amount to principal each month. Browse the full finance calculator suite to find tools for loan comparison, interest tracking, and more. No software needed, and everything is free.

FAQ

What is a mortgage statement?

A mortgage statement is a monthly document from your loan servicer that shows your payment due, outstanding loan balance, interest rate, payment allocation, and escrow activity. It gives you a full picture of your loan's current status.

What does PITI mean on a mortgage statement?

PITI stands for Principal, Interest, Taxes, and Insurance. These four components make up your total monthly mortgage payment, with taxes and insurance collected through an escrow account managed by your servicer.

Why did my mortgage payment increase?

Your payment can increase due to an escrow shortage from rising property taxes or insurance premiums, an adjustable rate adjustment, or a lender under-collection from a prior year. Check your statement's escrow section and lender messages for an explanation.

What is the difference between a mortgage statement and a payoff statement?

A monthly mortgage statement shows your loan status and payment due. A payoff statement shows the exact amount required to pay off the loan in full by a specific date. You must request a payoff statement separately, and it is required when refinancing or selling.

How do I dispute an error on my mortgage statement?

Under Regulation X, you have the right to submit a written error notice to your servicer. Include your account number, the specific error, and supporting documentation. Your servicer is required to investigate and respond within a defined timeframe under federal law.