See how MIP affects your monthly payment

Model principal, interest, taxes, insurance, and mortgage insurance on your loan scenario.

Open Mortgage Payment calculatorTL;DR:

- Mortgage insurance premiums (MIP) increase borrowing costs and monthly payments, especially when down payments are less than 20%.

- They primarily protect lenders and can often be eliminated through increased equity, refinancing, or waiting until thresholds are met.

- Viewing MIP as a temporary tool with a clear removal plan helps buyers build equity sooner and avoid paying premiums indefinitely.

Most homebuyers see mortgage insurance premium as nothing more than an extra charge tacked onto their monthly bill. That assumption leads many people to either delay buying a home or make financial decisions that cost more in the long run. In reality, mortgage insurance premium affects how much you can borrow, which loan programs you qualify for, and how quickly you can build equity. Understanding how it works, what drives the cost, and how to manage or eliminate it gives you a real advantage when shopping for a home or refinancing an existing loan.

Key Takeaways

| Point | Details |

|---|---|

| MIP protects lenders | Mortgage insurance premiums shield lenders from risk if the buyer defaults. |

| Impacts overall cost | MIP can add thousands to your total loan cost, especially with lower down payments. |

| Removable with equity | Once you own 20% of your home, you may remove MIP and cut your monthly payments. |

| Smart use can boost ownership | Treating MIP as a stepping stone lets buyers start earlier and plan for strategic removal. |

How mortgage insurance premiums influence your loan and monthly payments

The practical impact of MIP shows up immediately in your monthly payment. For FHA loans, the annual MIP rate in 2026 typically ranges from 0.55% to 1.05% of the loan balance, depending on the loan term and amount. That cost is divided by 12 and added to your monthly payment.

Here is a side-by-side comparison showing the real cost difference between a 5% down payment and a 20% down payment on a $350,000 home:

| Scenario | Down payment | Loan amount | Estimated MIP (annual) | Monthly MIP added | Total extra cost over 7 years |

|---|---|---|---|---|---|

| 5% down (FHA) | $17,500 | $332,500 | ~$1,829 (0.55%) | ~$152 | ~$12,804 |

| 10% down (FHA) | $35,000 | $315,000 | ~$1,733 (0.55%) | ~$144 | ~$12,096 |

| 20% down (conventional) | $70,000 | $280,000 | None | $0 | $0 |

The numbers make the cost visible. A buyer putting 5% down on an FHA loan pays over $12,000 extra in MIP over seven years alone. That said, saving an additional $52,500 to reach 20% down on a $350,000 home could take years. For many buyers, paying MIP is the more practical path to ownership.

Key ways MIP affects your loan:

- It increases your effective monthly payment, which reduces the loan amount you can qualify for at a given income level

- It raises your total cost of borrowing, similar in effect to a slightly higher interest rate

- FHA MIP includes an upfront premium of 1.75% of the loan amount, paid at closing or rolled into the loan balance

- PMI on conventional loans can sometimes be paid as a lump sum upfront or as a slightly higher interest rate through lender-paid PMI

Using a mortgage payment calculator helps you model both scenarios accurately before you commit to a loan program. Seeing the actual monthly numbers side by side removes guesswork and supports better decision-making.

The long-term impact is often underestimated. Over a 30-year FHA loan where MIP never drops off, a buyer could pay tens of thousands of dollars in cumulative insurance premiums. Loan type selection and down payment strategy directly shape that outcome.

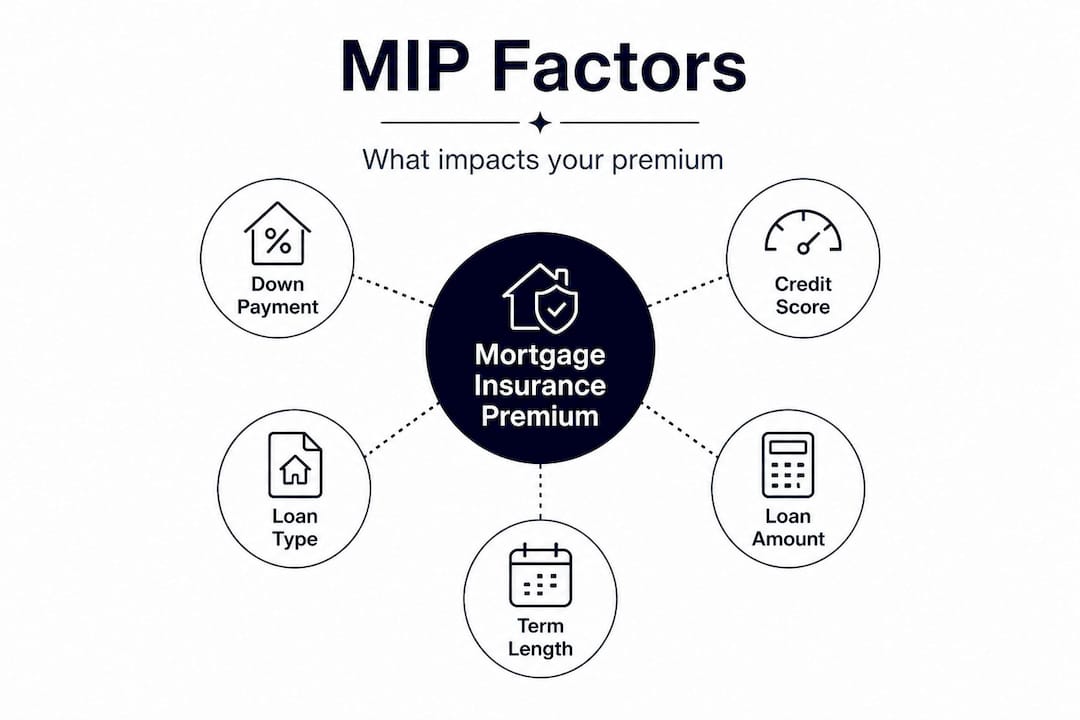

Factors that determine your mortgage insurance premium

Not every borrower pays the same MIP rate. Several variables interact to set your specific premium, and understanding them helps you take steps to lower your cost before you apply.

The main factors that influence MIP:

- Down payment amount: The larger your down payment, the lower your loan-to-value ratio (LTV), and typically the lower your MIP rate. Crossing key thresholds like 5%, 10%, or 20% down can move you into a lower premium tier or eliminate MIP entirely.

- Credit score: For conventional loans with PMI, a higher credit score directly reduces your PMI rate. Lenders view high credit scores as lower default risk, and private insurers price accordingly. FHA MIP rates are not as directly tied to credit scores, but your credit score still affects your interest rate.

- Loan type: FHA, conventional, USDA, and VA loans each follow different insurance rules. FHA MIP is mandatory regardless of down payment. Conventional PMI is required only when LTV exceeds 80%. USDA loans carry a 1% upfront guarantee fee plus 0.35% annual fee.

- Loan term: FHA MIP rates are lower for 15-year loans than for 30-year loans. Choosing a shorter loan term saves on both interest and insurance costs.

- Property type: Condominiums and multi-unit properties can carry slightly different rates, particularly with FHA financing.

| Factor | Effect on MIP |

|---|---|

| Down payment below 10% | Higher MIP rate |

| Down payment 10% or more | Lower MIP rate for FHA |

| Down payment 20% or more | No PMI on conventional loans |

| Credit score above 760 | Lowest PMI rates on conventional |

| 30-year vs. 15-year term | Higher MIP on 30-year FHA |

When estimating mortgage payments before you apply, factor in both the base loan payment and the MIP cost. Many buyers focus only on the principal and interest and miss how much insurance adds to the total. A loan payment calculator can show you exactly how each variable changes your payment. You can also use a compound interest calculator to model the long-term cost of rolling your upfront FHA MIP into the loan balance, since that added amount accrues interest over the life of the loan.

Pro Tip: Raising your credit score by even 40 to 60 points before applying for a conventional loan can meaningfully reduce your PMI rate. Pull your credit report, dispute any errors, and pay down revolving balances to boost your score before you shop.

Explore calculators and tools for smarter mortgage decisions

Understanding MIP is one thing. Seeing exactly how it affects your specific loan, payment, and long-term costs is something our tools make simple and immediate.

HelpCalculate.com gives you access to a full suite of mortgage calculators designed for homebuyers, current homeowners, and investors who want to model real scenarios. You can calculate the impact of extra payments on your payoff timeline, compare FHA versus conventional loan costs side by side, and estimate when you can drop MIP. The platform also offers finance widgets that embed directly into financial planning workflows, so you always have the tools you need without switching between apps. Whether you are preparing to buy, planning a refinance, or optimizing an existing mortgage, these tools put the numbers in your hands immediately.

FAQ

When can you stop paying mortgage insurance premiums?

You can often stop paying when you reach 20% home equity, but timing depends on your loan type and lender rules. FHA loans originated with less than 10% down require MIP for the full loan term unless you refinance.

Is mortgage insurance premium tax deductible?

Mortgage insurance premiums may be tax deductible, but it depends on current IRS guidelines and annual tax updates. Check with a qualified tax professional for guidance specific to your situation and filing year.

How much does mortgage insurance premium cost?

MIP typically costs between 0.5% and 1% of your loan amount yearly, depending on factors like down payment and credit score. FHA loans also carry an upfront MIP of 1.75% of the loan amount at closing.

Can you refinance to remove mortgage insurance premiums?

Yes, refinancing into a conventional loan once you have 20% equity allows many FHA homeowners to drop MIP entirely and potentially lower their interest rate at the same time.

Does every mortgage require insurance premium?

No, conventional loans with a 20% down payment generally do not require MIP, and VA loans for eligible veterans are exempt entirely. FHA and USDA loans do require some form of mortgage insurance regardless of down payment size.