Estimate your full monthly mortgage payment

Enter loan amount, rate, taxes, and insurance to see principal, interest, and PITI in seconds.

Open Mortgage Payment calculatorTL;DR:

- Calculating your mortgage payment requires accurate inputs such as loan amount, interest rate, and loan term to avoid errors.

- Using online calculators or financial tools simplifies the process and helps model various scenarios for better financial planning.

- Regularly reviewing and adjusting your mortgage strategy can save you thousands of dollars over the life of your loan.

Figuring out your monthly mortgage payment can feel overwhelming, especially when lenders throw around terms like amortization, principal, and escrow without much explanation. Most people sign a 30-year commitment without fully understanding what drives that monthly number or how changing one variable can shift it significantly. This guide walks you through exactly what information you need, how the math works, and how to verify your results, so you can approach any home financing decision with clarity and confidence.

Key Takeaways

| Point | Details |

|---|---|

| Get your numbers ready | Accurate loan details and costs are crucial for correct mortgage calculations. |

| Use step-by-step methods | Follow a clear process or trusted calculator to determine your monthly payment easily. |

| Check for mistakes | Verify results using multiple tools to avoid costly errors. |

| Small changes matter | Minor adjustments to your loan, rate, or payments can lead to big savings over time. |

| Leverage calculators | Online calculators simplify the math and help you plan smarter home financing. |

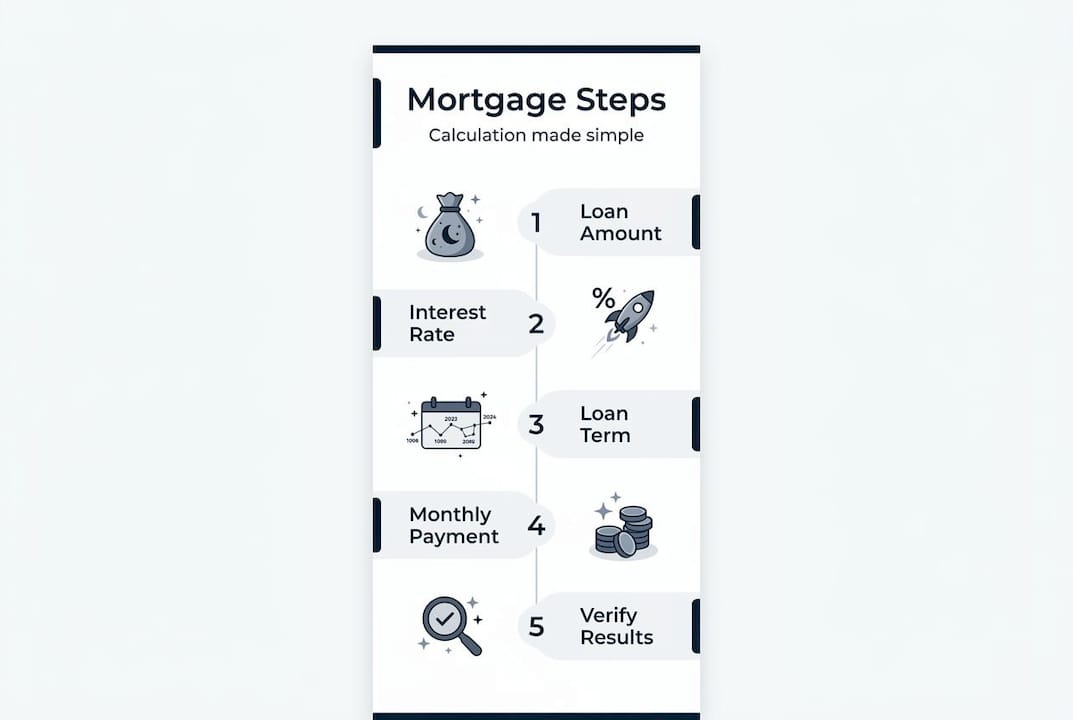

What you need before calculating your mortgage

Now that you know why mortgage math is essential, let's gather everything you'll need to calculate confidently. Jumping into calculations without the right inputs is the number one reason people end up with inaccurate estimates. Being organized upfront saves time and prevents costly mistakes down the line.

Core information you need

Here is the complete list of inputs required to calculate your monthly mortgage payment accurately:

- •Loan amount: The total amount you plan to borrow, which is the home purchase price minus your down payment. For example, if the home costs $350,000 and you put down $70,000 (20%), your loan amount is $280,000.

- •Interest rate: The annual interest rate your lender quotes you. This is not the APR (Annual Percentage Rate), which includes fees. You need the base interest rate for the formula.

- •Loan term: The number of years you will repay the loan. Common terms are 15 years and 30 years.

- •Property taxes: Your local tax authority sets this. It is usually calculated annually and divided by 12 for monthly estimates.

- •Homeowner's insurance: Your lender typically requires this. Average annual premiums vary widely by state and coverage level.

- •HOA fees: If your property is in a homeowners association, include the monthly dues. Not all properties carry this cost.

Tools you can use

You have two main options for calculating your mortgage. You can work through the amortization formula manually with a standard scientific calculator, or you can use purpose-built finance widgets designed specifically for mortgage math. Online tools are faster, reduce errors, and let you test multiple scenarios in seconds. For most homeowners, a dedicated mortgage payment calculator is the most practical starting point.

If you also want to compare loan types or estimate costs on personal loans alongside your mortgage, a loan payment calculator covers those scenarios too.

Quick reference: Required inputs at a glance

| Input | Example value | Where to find it |

|---|---|---|

| Loan amount | $280,000 | Purchase price minus down payment |

| Annual interest rate | 6.75% | Lender quote or mortgage offer letter |

| Loan term | 30 years (360 months) | Your loan agreement |

| Annual property tax | $4,200 | County assessor's website |

| Annual homeowner's insurance | $1,500 | Insurance quote or policy |

| Monthly HOA fee | $250 | HOA disclosure documents |

Pro Tip: Always confirm whether your lender quoted you an annual or monthly rate. The amortization formula uses a monthly rate, which is the annual rate divided by 12. Using the annual rate directly without converting it is one of the most common errors in manual calculations.

Step-by-step: How to calculate your monthly mortgage payment

With all your pieces in place, it's time to run the numbers and see what your monthly payment actually looks like. This section covers both the manual formula and the faster calculator method.

The amortization formula explained

The standard amortization formula calculates your fixed principal and interest payment. Here it is written out plainly:

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Each variable has a specific meaning:

- •M = Monthly payment (what you're solving for)

- •P = Principal loan amount (e.g., $280,000)

- •r = Monthly interest rate (annual rate ÷ 12; so 6.75% ÷ 12 = 0.5625% or 0.005625)

- •n = Total number of payments (30 years × 12 months = 360)

This is the detailed process for calculating monthly payments that underpins every mortgage estimate you see online.

Step-by-step calculation walkthrough

Follow these steps using the sample numbers from our table above:

- Identify your loan amount (P): $280,000

- Convert your annual rate to monthly (r): 6.75% ÷ 12 = 0.5625% = 0.005625

- Calculate your total number of payments (n): 30 × 12 = 360

- Plug into the formula: M = 280,000 × [0.005625 × (1.005625)^360] / [(1.005625)^360 - 1]

- Solve the exponent: (1.005625)^360 ≈ 7.6876

- Complete the numerator: 0.005625 × 7.6876 ≈ 0.04324

- Complete the denominator: 7.6876 - 1 = 6.6876

- Divide and multiply: 0.04324 / 6.6876 ≈ 0.006466; then 280,000 × 0.006466 ≈ $1,810.47

That $1,810.47 is your base principal and interest payment only. Add your monthly property tax ($4,200 ÷ 12 = $350), insurance ($1,500 ÷ 12 = $125), and HOA fees ($250) to get your full PITI (Principal, Interest, Taxes, Insurance) payment of approximately $2,535.47 per month.

Manual vs. calculator comparison

| Method | Time required | Error risk | Scenario testing |

|---|---|---|---|

| Manual formula | 10 to 15 minutes | High (one wrong decimal ruins it) | Slow, one at a time |

| Online calculator | Under 1 minute | Very low | Fast, multiple scenarios |

| Spreadsheet model | 5 to 10 minutes | Medium | Good for detailed analysis |

Pro Tip: For most homeowners, running your numbers through a simple mortgage payment estimator first and then double-checking with the formula is the most reliable approach. Calculators handle the exponent math instantly and eliminate rounding errors. You can also explore other finance calculators to run scenarios on refinancing, extra payments, or total loan cost comparisons.

Verifying your results: Common calculation mistakes and how to avoid them

After running the numbers, it's wise to check your work and ensure your calculations are both accurate and realistic. Even small errors in the inputs can result in payment estimates that are hundreds of dollars off each month.

Mistakes to check for immediately

- •Using the annual rate instead of the monthly rate: This is the single most common manual error. Always divide your annual rate by 12 before plugging it into the formula.

- •Forgetting to convert years to months: The formula requires total payments in months, not years. A 30-year loan is 360 payments, not 30.

- •Leaving out taxes and insurance: Many online calculators default to principal and interest only. Your actual monthly obligation includes property taxes, homeowner's insurance, and HOA fees where applicable.

- •Using the listing price instead of the loan amount: Your loan amount is what you borrow after the down payment, not the full home price.

- •Assuming the lender's quoted payment includes everything: Some lender estimates show only P&I. Always ask what is and is not included in any payment quote you receive.

- •Not accounting for private mortgage insurance (PMI): If your down payment is less than 20%, your lender will typically require PMI, which adds a monthly cost to your payment.

Why recalculating after changes matters

If anything in your financial picture changes, including a rate lock update, a different down payment amount, or a change in property tax assessment, you need to recalculate from scratch. A 0.5% increase in your interest rate on a $280,000 loan over 30 years adds roughly $90 per month to your payment, and more than $32,000 in total interest over the life of the loan. That is not a rounding error. It is a material difference.

Exploring the extra payment impact on your loan is especially useful if you plan to pay more than the minimum. Even $100 extra per month can reduce your loan term by several years.

Next-level mortgage insights: How small changes impact your payment

Understanding your base payment is powerful, but seeing how tweaks can save money or time makes you a true mortgage pro. The relationship between rate, term, and total cost is not always intuitive, and the numbers can surprise you.

How rate, term, and extra payments shift your costs

The table below uses a $280,000 loan to show how different scenarios affect your monthly payment and total interest paid over the life of the loan. These figures represent principal and interest only, using finance calculators as reference tools.

| Scenario | Rate | Term | Monthly P&I | Total interest paid |

|---|---|---|---|---|

| Base case | 6.75% | 30 years | $1,810.47 | $371,769 |

| Lower rate | 6.25% | 30 years | $1,724.19 | $340,708 |

| Shorter term | 6.75% | 15 years | $2,476.08 | $165,694 |

| Extra $200/month | 6.75% | ~25 years | $2,010.47 | ~$295,000 |

The savings are striking. Dropping your rate by just 0.5% saves you over $31,000 in interest. Choosing a 15-year term over a 30-year term saves more than $206,000 in interest, though it raises your monthly payment by around $665. Adding $200 per month to your base payment shaves approximately five years off the loan and saves close to $77,000 in interest. Explore loan calculators to model any of these scenarios with your actual numbers.

Actionable ways to reduce your total mortgage cost

- •Negotiate your rate: Even a 0.25% rate reduction is worth pursuing. On a $280,000 loan, that difference compounds to tens of thousands over 30 years.

- •Make biweekly payments: Paying half your monthly payment every two weeks results in one extra full payment per year, reducing interest accumulation.

- •Put extra payments toward principal only: Specify to your lender that any extra payments should be applied to principal, not future payments, to maximize interest savings.

- •Refinance when rates drop: If rates fall 1% or more below your current rate and you plan to stay in the home for several years, refinancing can be cost effective.

- •Increase your down payment: Going from 10% to 20% down reduces your loan amount, eliminates PMI, and can improve your rate offer from lenders.

- •Shorten your loan term at renewal or refinance: Moving from a 30-year to a 20-year mortgage reduces total interest even if the rate stays the same.

Check the extra mortgage payment calculator to see exactly how much your extra payments would save based on your specific loan balance and rate.

The truth about mortgages: Why the formula is only half the story

Most people treat mortgage math as a one-time calculation done when they apply for a loan. That is a mistake. Your mortgage should be a living financial tool you review regularly, not a number you set and forget for 30 years.

The formula gives you the payment. What it does not give you is context. Plenty of homeowners fixate on nailing every decimal in the amortization formula while leaving far bigger opportunities on the table. Negotiating just 0.375% off your interest rate can save you more money than years of perfect payment tracking. Understanding when to refinance, whether to make extra payments, or how a home equity line of credit affects your position is worth far more than manual formula precision.

Behavior matters as much as math. Research consistently shows that homeowners who revisit their mortgage terms annually, whether that means refinancing, adjusting extra payment amounts, or comparing their rate to current market rates, end up paying tens of thousands less over the life of their loan. The formula does not track that for you. You have to make it a practice.

We also see people get overwhelmed by complexity and do nothing. That is the worst outcome. Running a quick estimate using the best finance calculators for homeowners takes two minutes and can immediately show whether your current strategy is optimal or whether you should reconsider your term, rate, or payment structure.

Pro Tip: Set a calendar reminder once a year to re-run your mortgage scenario with current market rates. If rates have fallen significantly, a refinance conversation with your lender may be worth having. If you have made extra payments, update your calculator inputs to see your new projected payoff date. Mortgage calculations are not a one-time exercise.

Calculate smarter with our free mortgage and finance tools

Knowing the formula and theory is valuable. Having the right tools to apply that knowledge instantly is even better.

At HelpCalculate.com, our suite of mortgage calculators makes it easy to estimate your monthly payment, model different scenarios, and verify your math without needing a spreadsheet or financial background. Whether you are comparing a 15-year versus 30-year term, checking the impact of extra payments, or estimating total interest, our tools deliver clear results in seconds. You can also explore our math calculators for general financial arithmetic and our embeddable finance widgets if you want to run calculations from any device or website. Accurate mortgage math is always just a click away.

FAQ

What is the formula to calculate a mortgage payment?

The standard loan amortization formula, M = P × [r(1+r)^n] / [(1+r)^n - 1], uses your loan amount, monthly interest rate, and total number of payments to determine your fixed monthly cost. You can also use the mortgage payment calculator to get instant results without manual calculation.

What fees and costs are included in a typical mortgage payment?

A standard mortgage payment includes principal, interest, property taxes, and homeowner's insurance, collectively known as PITI. Some payments also include HOA fees or PMI, and these are factored into the full estimate by finance tools that account for all four cost components.

How can I quickly check my mortgage math for mistakes?

Run your calculation in two separate tools and compare the outputs. If the results differ, recheck your inputs, particularly the interest rate format and whether you converted years to months. Finance calculators help confirm accuracy quickly.

Do extra mortgage payments really reduce the total interest?

Yes. Extra payments applied directly to principal reduce the outstanding balance faster, which lowers the amount of interest that accrues each month. Over time, this can save tens of thousands of dollars and shorten the loan term by several years. Finance tools can model the exact impact for your loan.

Where can I find a free online mortgage calculator?

A free, accurate option is available at HelpCalculate.com, which estimates your full monthly payment including principal, interest, taxes, and insurance with no sign-up required.