TL;DR:

- Knowing your home equity is essential for making confident financial decisions, as it influences refinancing, loans, and sales.

- Accurate calculations require current market value and precise payoff amounts, with professional appraisals and direct lender confirmation providing the most reliable data.

- Most lenders limit borrowing to 80-85% of your home value, making understanding accessible and total equity crucial for planning.

Knowing your home equity is the difference between making a confident financial decision and guessing. Whether you’re considering a cash-out refinance, applying for a home equity loan, or preparing to sell, your equity number drives everything. This calculate home equity guide walks you through exactly what you need: the right data to gather, the home equity formula to apply, and the common mistakes that throw off your numbers. American homeowners collectively hold over $17 trillion in home equity as of Q3 2025. Knowing your share of that figure starts here.

Key Takeaways

| Point | Details |

|---|---|

| Use the right formula | Home equity equals current market value minus all outstanding debt secured by the home. |

| Get the payoff amount | The payoff figure from your lender is always more accurate than the balance on your monthly statement. |

| Watch your accessible equity | Lenders typically require you to retain 15–20% equity, so borrowable amounts are less than total equity. |

| Online estimates have limits | Automated valuations can be off by 5% or more; a professional appraisal gives lenders what they need. |

| LTV ratio shapes your options | Your loan-to-value ratio determines borrowing power and interest rates, not just equity in dollar terms. |

What you need before calculating home equity

You cannot run an accurate calculation without two reliable numbers: your home’s current market value and the total outstanding debt secured by the property. Getting either one wrong skews everything that follows.

Estimating your home’s current value

Several methods exist, and they vary in accuracy and cost.

- Online automated valuation tools (such as Zillow’s Zestimate or Redfin’s estimate) pull recent sales data and tax records to produce instant numbers. They are convenient but can carry meaningful error margins. Automated values can be off by 5%+, which on a $400,000 home means a $20,000 swing in either direction.

- County assessor records reflect the assessed value for tax purposes, which often lags actual market conditions by one to three years. Use these for reference only.

- Comparative market analysis (CMA) from a licensed real estate agent is free and more current. An agent pulls recent sales of similar homes in your neighborhood and adjusts for differences in size, condition, and features.

- Formal appraisal is the gold standard. Professional appraisals cost $300 to $500 but produce a defensible figure that any lender will accept.

For planning purposes, a CMA works well. For actual loan applications, expect the lender to order their own appraisal regardless.

Finding your total outstanding debt

This step trips up more homeowners than the valuation side. You need the balances on every loan secured by your home, not just your primary mortgage.

- Primary mortgage: Log into your servicer’s online portal or check your most recent statement for the current principal balance.

- Second mortgage: Include the full outstanding balance if you have one.

- HELOC (Home Equity Line of Credit): Only count the amount actually drawn, not the total credit limit approved. If your HELOC allows up to $80,000 but you’ve drawn $30,000, your debt figure is $30,000.

- Payoff amount vs. statement balance: Your monthly statement balance does not capture accrued interest or any prepayment penalties. The payoff amount from your lender is what you actually owe on a specific payoff date. Always request this directly from your servicer when precision matters.

Pro Tip: Call your mortgage servicer and request a formal payoff statement. Most servicers provide this within one to three business days at no charge. Use this figure instead of your statement balance for any equity calculation that affects a financial decision.

How to calculate equity step by step

With accurate inputs in hand, the math is straightforward. Here is how to work through it.

The core home equity formula

Home Equity = Current Fair Market Value − Total Outstanding Debt Secured by the Home

Using percentages: (Total Equity / Current Home Value) × 100 = Equity Percentage

And for LTV: (Total Debt / Appraised Value) × 100 = LTV%

A worked example

- Confirm your home’s current market value. For this example: $450,000.

- Add up all secured debt. Primary mortgage payoff amount: $280,000. HELOC drawn balance: $20,000. Total debt: $300,000.

- Apply the formula: $450,000 − $300,000 = $150,000 total equity.

- Calculate your equity percentage: ($150,000 / $450,000) × 100 = 33.3%.

- Calculate LTV: ($300,000 / $450,000) × 100 = 66.7% LTV.

That 33.3% equity stake sounds solid. But how much of it can you actually borrow against?

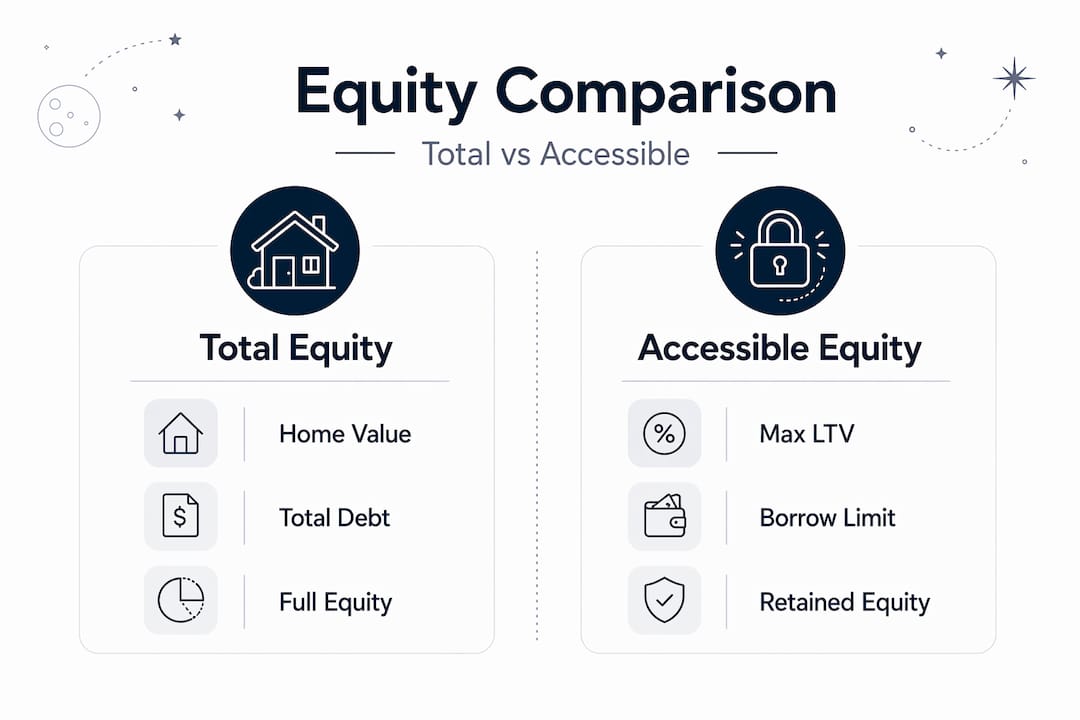

Total equity vs. accessible equity

Lenders cap LTV ratios at roughly 80% to 85%, which means they require you to retain at least 15% to 20% equity after any new borrowing. Here is how that plays out in the example above.

| Scenario | Home Value | Total Debt | Total Equity | Max LTV (80%) | Max New Borrowing |

|---|---|---|---|---|---|

| Example homeowner | $450,000 | $300,000 | $150,000 (33.3%) | $360,000 | $60,000 |

| Higher debt scenario | $450,000 | $380,000 | $70,000 (15.6%) | $360,000 | $0 (at limit) |

| More equity scenario | $450,000 | $200,000 | $250,000 (55.6%) | $360,000 | $160,000 |

The table makes it clear: total equity and accessible equity are not the same number. Your borrowing power depends on where your current debt sits relative to the lender’s LTV ceiling, not on your raw equity figure alone.

Common pitfalls and how to avoid them

Understanding the home equity formula is one thing. Applying it accurately in the real world requires navigating several practical challenges.

Valuation gaps and market timing

Online automated valuations are useful starting points, but appraisal-based valuations better reflect market nuances than algorithmic estimates. A recent kitchen renovation or a newly constructed school two blocks away may not factor into an automated tool but absolutely affects what a buyer would pay.

Local market conditions also shift quickly. A home valued at $420,000 in spring may appraise at $400,000 by fall if inventory rises or interest rates cool demand. If you’re timing a refinance or sale, track your local market monthly, not annually.

- Use at least two valuation sources and compare them before making a decision.

- If the two estimates differ by more than 5%, prioritize the CMA or appraisal.

- Factor in the cost and time of major renovations versus their likely impact on appraised value before borrowing to fund them.

Debt calculation errors

The payoff amount issue deserves repetition because it is the most common error homeowners make. Your statement says you owe $185,000, so you plan around that. But your actual payoff, including accrued interest since the last payment cycle, may be $185,700. On a closing table, that $700 difference can stall a deal. Always obtain the payoff figure directly from the lender and confirm the date through which it is valid.

Loan eligibility beyond equity numbers

Equity alone does not guarantee loan approval. Lenders consider LTV ratios alongside debt-to-income ratios when setting terms and deciding whether to approve a loan. A homeowner with strong equity but a 50% DTI ratio may face higher rates or denial. Credit score requirements typically start at 620 to 640, and maximum DTI ratios are often capped at 45%.

Home equity gives you access to financial tools, but lenders evaluate the full picture. A strong equity position combined with a high debt load can still result in unfavorable loan terms or rejection.

Pro Tip: Before applying for any home equity product, pull your credit report and calculate your DTI (monthly debt payments divided by gross monthly income). Address any issues there first. A cleaner financial profile means better rates even when your equity is strong.

Putting your equity number to work

Once you know your equity, you have several paths forward. Each one uses your equity calculation differently.

-

Home equity loan: You borrow a fixed lump sum against your equity, repaid at a fixed rate over a set term. The lender calculates how much you can borrow using CLTV. For types of home equity loans and how they are structured, reviewing a detailed breakdown helps you compare options before applying.

-

HELOC: A revolving credit line secured by your home. You draw what you need, repay it, and draw again during the draw period. Only your drawn balance counts against your equity in future calculations.

-

Cash-out refinance: You replace your existing mortgage with a new, larger one and take the difference in cash. This resets your loan term and may change your rate. Use this when current rates are lower than your existing rate or when you need a large lump sum.

-

Selling the home: Your equity translates directly to net proceeds after paying off all liens and covering closing costs, agent commissions (typically 5% to 6% of sale price), and any outstanding taxes or fees.

| Equity Access Method | How equity is used | Key cost consideration |

|---|---|---|

| Home equity loan | Fixed lump sum borrowing | Closing costs of 2% to 5% of loan amount |

| HELOC | Revolving credit line | Variable rates; only drawn balance counts as debt |

| Cash-out refinance | New larger mortgage | New loan origination costs; rate change risk |

| Home sale | Full equity realized | Agent commissions, closing costs, lien payoffs |

For any borrowing option, lenders use LTV as a primary risk metric rather than raw equity dollars. Two homeowners with identical equity amounts but different LTV ratios will receive different offers. Running the numbers with a loan payment calculator before applying helps you see what monthly payments would look like at various loan amounts and rates. If you’re weighing a home equity loan against refinancing, understanding the trade-offs in depth matters. Comparing a home equity loan or refinance as debt solutions shows you how lenders structure these products differently.

My take on calculating home equity accurately

I’ve worked with enough financial data and homeowners over the years to say this plainly: the biggest equity calculation mistakes are not math errors. They are data errors.

The homeowner who plugs in an online Zestimate from six months ago and a statement balance instead of a payoff amount can end up with an equity figure that’s $15,000 to $25,000 off. That gap is not academic. It affects what loan products you qualify for, how you price your home for sale, and whether a refinance makes financial sense.

What I’ve found is that most people skip the payoff amount step because calling the servicer feels like extra work. It takes about 10 minutes. For any decision involving real money, that 10 minutes is worth it every time.

I also think homeowners underestimate how much lender policies vary. Two lenders may both advertise 80% LTV limits, but one may use an automated valuation for the appraisal while the other requires a full in-person appraisal. That difference alone can change the equity value they recognize by thousands of dollars. Understanding home equity calculations is the foundation, but working directly with your lender to confirm their inputs is what ties the math to reality.

My honest advice: run your own calculation first using accurate figures, then use a calculator tool to cross-check it, and then have a lender confirm it before making any financial move.

— Michael

Calculate equity with free tools from Helpcalculate

Helpcalculate offers a full suite of free finance calculators that homeowners can use to run equity calculations, model loan scenarios, and estimate monthly payments without needing a spreadsheet or financial advisor on call. The loan payment calculator lets you plug in a loan amount, term, and interest rate to see what a home equity loan would actually cost you per month. The math and percentage tools help you verify LTV and equity percentages without rounding errors. You can also explore embeddable finance widgets if you want to keep these tools accessible on your own site or reference page. Cross-checking your manual calculations against these tools takes minutes and catches errors before they affect a real decision.

FAQ

What is the basic home equity formula?

Home equity equals your home's current fair market value minus the total outstanding debt secured by the property, including all mortgages and HELOCs.

How do I find my accurate payoff amount?

Contact your mortgage servicer directly and request a formal payoff statement. This figure includes accrued interest and any penalties, making it more accurate than your monthly statement balance.

How much of my equity can I actually borrow?

Most lenders cap borrowing at 80% to 85% of your home's appraised value combined across all loans, meaning you must retain at least 15% to 20% equity after any new loan.

Does my credit score affect home equity loan eligibility?

Yes. Credit score requirements typically start at 620 to 640, and lenders also evaluate your debt-to-income ratio, which is generally capped at 45%, alongside your equity position.

Are online home equity estimators accurate enough to use?

They work well for general planning but should not be used as your final number. Automated valuations can be off by 5% or more, and lenders will order their own appraisal regardless.

Recommended on Help Calculate

- •Home affordability calculator - price range by income (2026) | Help Calculate

- •Extra mortgage payment calculator - interest saved & payoff date | Help Calculate

- •Loan payment calculator - monthly payment & interest | Help Calculate

- •Mortgage payment calculator - estimate PITI & monthly cost | Help Calculate