Calculate Your Exact Car Budget

Enter your income, debts, and down payment to get your personalized recommendation in 30 seconds.

Open car affordability calculatorYour Take-Home Pay Reality on $50,000

Before we calculate anything, let's be honest about what you're actually bringing home.

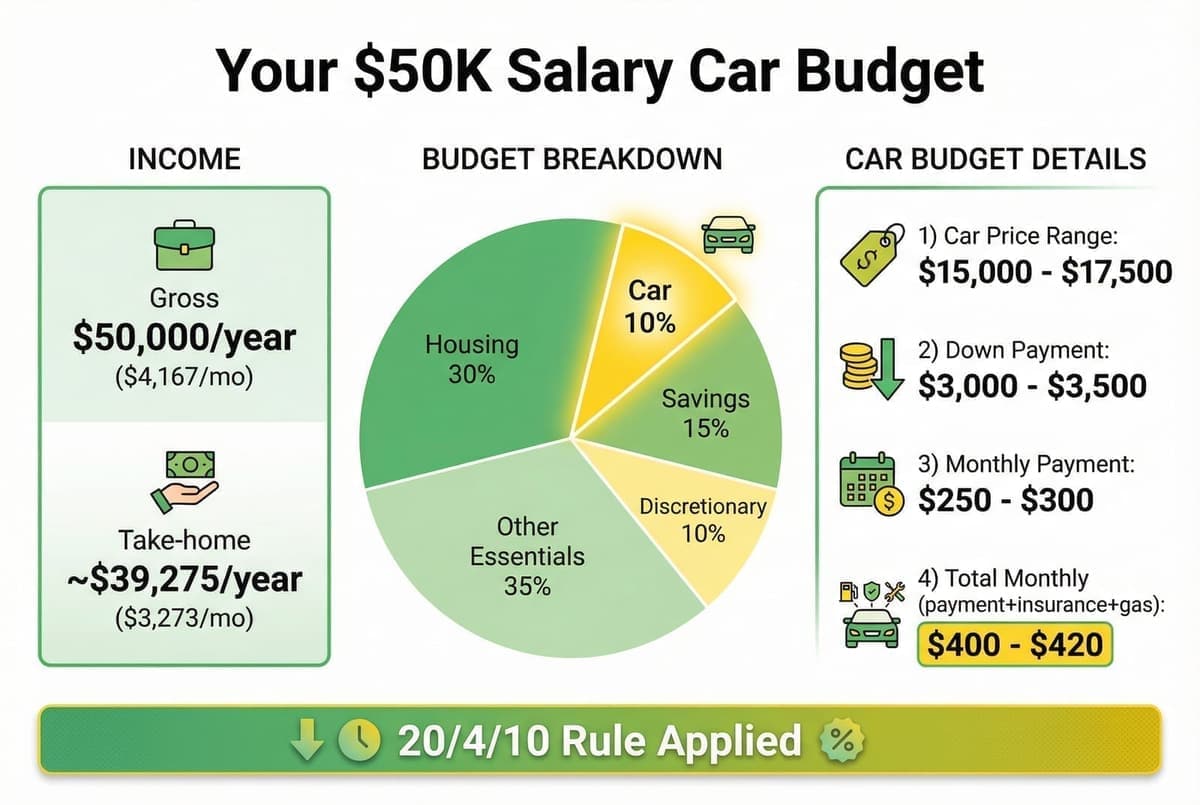

Gross Income: $50,000/year. Monthly Gross: $4,167.

After taxes and deductions: Federal tax ~$4,200/year, FICA (Social Security + Medicare) ~$3,825/year, State tax ~$1,500/year (varies by state), Health insurance ~$1,200/year (if not employer-covered).

Estimated Annual Take-Home: ~$39,275. Monthly Take-Home: ~$3,273.

This is the real number we're working with. Not $4,167. Any car payment needs to fit into your $3,273 monthly budget, not the higher gross number dealers will use.

The 20/4/10 Rule Applied to Your $50K Salary

The 20/4/10 rule is the gold standard for car affordability.

20% Down Payment

Put at least 20% down to avoid being underwater on your loan immediately. For a $20,000 car: $4,000 down payment.

4-Year (48-Month) Loan Maximum

Stretch beyond 48 months and you're paying excessive interest and risking negative equity. Loan term: 48 months max (not 60, 72, or 84 months).

10% of Gross Monthly Income

Your total car expenses (payment + insurance + gas + maintenance) should not exceed 10% of your gross monthly income. 10% of $4,167 = $417/month maximum for ALL car expenses.

Breaking this down: Car payment ~$280/month, Insurance ~$80/month, Gas ~$40/month (if you don't drive much), Maintenance ~$17/month average. This is tight but doable if you choose wisely.

What Car Price Can You Afford? The Math

Let's calculate your realistic price range using two different approaches.

Method 1: The 10% Rule

If you can spend $417/month total on car expenses, and your payment should be about 65–70% of that: Maximum monthly payment ~$280. Loan amount at 7% APR for 48 months ~$12,000. Add 20% down payment ($3,000). Maximum car price: ~$15,000.

Method 2: Income-Based Formula

Conservative guideline: Car price should not exceed 30–35% of your annual gross income. $50,000 × 30% = $15,000. $50,000 × 35% = $17,500. Your realistic car budget: $15,000–$18,000.

The Sweet Spot

Based on both methods, your ideal car budget is $15,000–$17,500, with $18,000–$20,000 being the absolute maximum if you have: very low other debts, excellent credit (lower interest rate), lower insurance costs, and minimal driving (low gas/maintenance).

Most $50K earners should aim for the $15,000–$17,500 range.

Monthly Payment Expectations (Real Numbers)

Real monthly payments at different price points with current 2026 interest rates.

| Car Price | Down (20%) | Loan | 48 mo @ 7% | Monthly Payment |

|---|---|---|---|---|

| $15,000 | $3,000 | $12,000 | 48 months | $287 |

| $17,500 | $3,500 | $14,000 | 48 months | $335 |

| $20,000 | $4,000 | $16,000 | 48 months | $383 |

Add insurance ($80–120/mo) and gas ($40–80/mo). Only the $15K and $17.5K options fit comfortably within the 10% rule.

Best Cars You Can Buy on a $50,000 Salary

Reliable, practical vehicles that fit your budget in 2026.

$12,000–$15,000 Range (Best Value)

- •Honda Civic (2016–2018) - $13K–$15K. Legendary reliability, 30+ MPG. Watch for higher mileage (under 80K miles).

- •Toyota Corolla (2015–2017) - $12K–$14.5K. Bulletproof reliability, excellent resale.

- •Mazda3 (2016–2018) - $12.5K–$15K. Fun to drive, upscale interior. Smaller backseat, firm ride.

- •Honda Fit (2015–2018) - $11K–$14K. Incredible cargo space, 35+ MPG. Road noise, basic interior.

- •Hyundai Elantra (2017–2019) - $12K–$15K. Great warranty if transferable, loaded features.

$15,000–$18,000 Range (Stretch Budget)

- •Honda Accord (2015–2017) - $15K–$17.5K. Midsize comfort, Honda reliability. Watch for CVT in some years.

- •Toyota Camry (2014–2016) - $14.5K–$17K. Ultimate reliability, comfortable, strong resale.

- •Subaru Impreza/Crosstrek (2015–2017) - $15K–$18K. AWD standard, good in snow. Head gasket issues on older models.

- •Mazda CX-5 (2014–2016) - $15.5K–$18K. Compact SUV, fun to drive. Lower MPG than sedans.

- •Honda CR-V (2012–2014) - $14K–$17K. Spacious, reliable. Older model years in this range.

Down Payment Strategy for Your Income Level

For a $15,000–$17,500 car, you need $3,000–$3,500 for a 20% down payment. Savings timeline: Save $250/month = 12–14 months; $350/month = 9–10 months; $500/month = 6–7 months.

- •Option 1: Cash savings (best) - Save up before you buy. Gives you negotiating power.

- •Option 2: Trade-in value - If your current car is worth $2,000–$4,000, use it as part of your down payment.

- •Option 3: Tax refund - Average refund ~$3,000. Perfect down payment amount.

- •Option 4: Side income - Dedicated down payment fund from gig work or selling items.

7 Mistakes to Avoid at the $50K Income Level

Mistake #1: Thinking "I Make $50K, I Can Afford a $30K Car"

At $30K, your payment would be $550–650/month, eating 17–20% of gross income. Stick to $15K–$18K max.

Mistake #2: Taking a 72 or 84-Month Loan

You pay thousands more in interest and stay underwater for years. 48 months maximum.

Mistake #3: Forgetting About Insurance

Add $100–150/month for insurance. Get quotes before buying.

Mistake #4: Buying New "Because Monthly Payments Are Similar"

New cars lose $5,000–$8,000 the moment you drive off. Buy 2–4 years used and let someone else eat the depreciation.

Mistake #5: Maxing Out the Dealer's Approved Amount

Banks approve you for what makes them money. Just because you're approved doesn't mean you should borrow it.

Mistake #6: Not Shopping Your Interest Rate

Get pre-approved at your credit union or bank before visiting dealers. Compare.

Mistake #7: Paying Sticker Price

Offer 10–15% below asking on used cars. Worst they say is no.

How to Stretch Your Budget Safely (If You Must)

- •Increase down payment to 30–35% to lower the loan and monthly payment.

- •Buy from a private seller - save 10–20% vs dealer.

- •Time your purchase: December/January, end of month, when new models arrive.

- •Consider Certified Pre-Owned for better rates and warranty.

- •Increase income first - side hustle, promotion, or tax refund - then expand budget naturally.

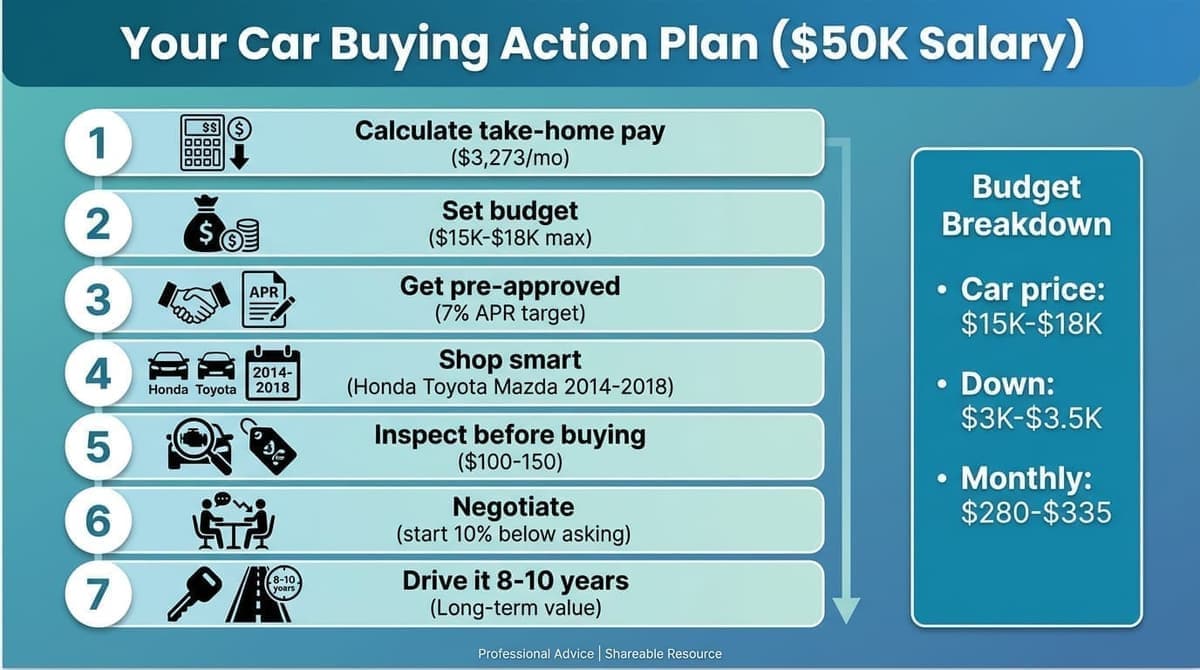

Your Action Plan: Next Steps

- •Calculate your exact take-home pay ($3,273/mo).

- •Set budget: $15K–$18K max.

- •Get pre-approved (target 7% APR).

- •Shop smart: Honda, Toyota, Mazda, Subaru 2014–2018.

- •Inspect before buying ($100–150).

- •Negotiate: start 10% below asking.

- •Drive it 8–10 years and build wealth.

Key takeaways

- •With $50K salary, aim for a $15,000–$17,500 car; $20K is the absolute max.

- •Follow the 20/4/10 rule: 20% down, 48-month loan, total car costs under 10% of gross income.

- •Monthly payment target: $280–$335. Add insurance and gas to stay under $417 total.

- •Best value: Honda Civic, Toyota Corolla, Mazda3, Honda Accord in the 2014–2018 range.

- •Avoid 72/84-month loans, dealer "approved" max, and skipping insurance in your budget.

Conclusion

Making $50K a year gives you solid car options -if you shop smart. Stick to the $15K–$18K range, finance for 48 months max, and you'll have a reliable car without the stress.

Use our car affordability calculator to see exactly what you can afford based on your income, debts, and down payment. Your future self (and bank account) will thank you.

FAQ

Can I afford a $25,000 car on $50,000 salary?

Technically possible but financially unwise. A $25K car with 20% down means ~$477/month payment alone; with insurance and gas you're at $600–650/month (19% of gross). Stick to $15K–$18K.

Should I lease or buy at this income level?

Buy. At $50K you need to build equity, not perpetual payments. Buy a reliable used car, pay it off in 4 years, then drive it payment-free for years.

What if I need a car NOW and only have $1,000 saved?

Options: buy a $5,000 beater with $1,000 down and save more for 6–12 months; delay and save aggressively 3–4 months; or minimum 10% down ($1,500–1,750) with higher payments.

Is it better to buy new with 0% financing or used with 7%?

Usually used. A new $28K car at 0% still loses ~$8K in year-one depreciation; a used $16K car at 7% loses ~$2K. The new car costs you thousands more overall.

How much should I spend on insurance?

Budget $80–150/month depending on age, driving record, location, and car type. Get quotes before buying.

Can I buy a truck or SUV at this income level?

Possible but challenging: higher mileage in your price range, lower MPG, higher insurance. If you need truck capability, look at older Tacoma, Ranger, or Frontier. Otherwise stick with sedans or small crossovers.

Should I pay cash or finance if I have the money saved?

At 7%+ rates, many advisors say put $5K down, finance $10K, and keep $10K for an emergency fund. You need an emergency fund more than avoiding $700–800 in interest over 4 years.

We are not financial advisors and everyone's situation is unique. This guide is intended to be helpful general information only. Always consult a qualified specialist if you need advice tailored to your circumstances.